The Generalized Lambda Distribution and GLDEX Package: Fitting Financial Return Data

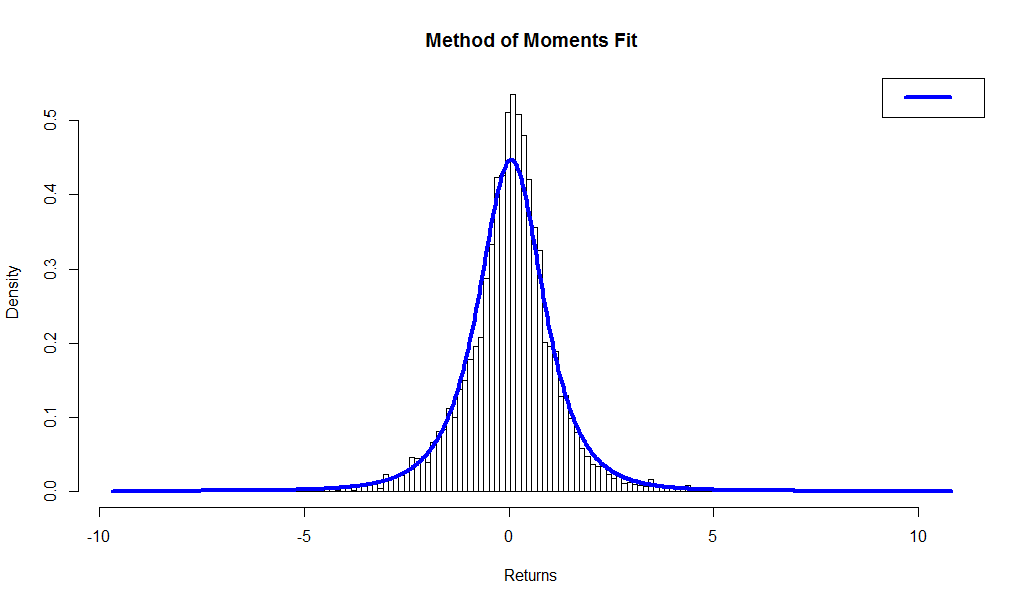

by Daniel Hanson, with contributions by Steve Su (author of the GLDEX package). Part 1 of a series. Introduction As most readers are well aware, market return data tends to have heavier tails than that which can be captured by a normal distribution; furthermore, skewness will not be captured either. For ...