ARIMA models and Intervention Analysis

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.

In my previous tutorial Structural Changes in Global Warming I introduced the strucchange package and some basic examples to date structural breaks in time series. In the present tutorial, I am going to show how dating structural changes (if any) and then Intervention Analysis can help in finding better ARIMA models. Dating structural changes consists in determining if there are any structural breaks in the time series data generating process, and, if so, their dates. Intervention analysis estimates the effect of an external or exogenous intervention on a time series. As an example of intervention, a permanent level shift, as we will see in this tutorial. In our scenario, the external or exogenous intervention is not known in advance, (or supposed to be known), it is inferred from the structural break we will identify.

The dataset considered for the analysis is the Arbuthnot dataset containing information of male and female births in London from year 1639 to 1710. Based on that, a metric representing the fractional excess of boys births versus girls is defined as:

$$

\begin{equation}

\begin{aligned}

\dfrac{(Boys – Girls)}{Girls}

\end{aligned}

\end{equation}

$$

The time series so defined is analyzed to determine candidate ARIMA models. The present tutorial is so organized. First, a brief exploratory analysis is carried on. Then, six ARIMA models are defined, analyzed and compared. Forecast of the time series under analysis is computed. Finally, a short historical background digression is introduced describing what was happening in England on 17-th century and citing studies on the matter of sex ratio at birth.

Packages

suppressPackageStartupMessages(library(ggplot2)) suppressPackageStartupMessages(library(forecast)) suppressPackageStartupMessages(library(astsa)) suppressPackageStartupMessages(library(lmtest)) suppressPackageStartupMessages(library(fUnitRoots)) suppressPackageStartupMessages(library(FitARMA)) suppressPackageStartupMessages(library(strucchange)) suppressPackageStartupMessages(library(reshape)) suppressPackageStartupMessages(library(Rmisc)) suppressPackageStartupMessages(library(fBasics))

Note:The fUnitRoots package is not any longer maintained by CRAN, however it can be installed from source available at the following link:

fUnitRoots version 3010.78 sources

Exploratory Analysis

Loading the Arbuthnot dataset and showing some basic metrics and plots.

url <- "https://www.openintro.org/stat/data/arbuthnot.csv"

abhutondot <- read.csv(url, header=TRUE)

nrow(abhutondot)

[1] 82

head(abhutondot)

year boys girls

1 1629 5218 4683

2 1630 4858 4457

3 1631 4422 4102

4 1632 4994 4590

5 1633 5158 4839

6 1634 5035 4820

abhutondot_rs <- melt(abhutondot, id = c("year"))

head(abhutondot_rs)

year variable value

1 1629 boys 5218

2 1630 boys 4858

3 1631 boys 4422

4 1632 boys 4994

5 1633 boys 5158

6 1634 boys 5035

tail(abhutondot_rs)

year variable value

159 1705 girls 7779

160 1706 girls 7417

161 1707 girls 7687

162 1708 girls 7623

163 1709 girls 7380

164 1710 girls 7288

ggplot(data = abhutondot_rs, aes(x = year)) + geom_line(aes(y = value, colour = variable)) +

scale_colour_manual(values = c("blue", "red"))

Gives this plot.

Boys births appear to be consistently greater than girls ones. Let us run a t.test to further verify if there is a true difference in the mean of the two groups as represented by boys and girls births.

t.test(value ~ variable, data = abhutondot_rs)

Welch Two Sample t-test

data: value by variable

t = 1.4697, df = 161.77, p-value = 0.1436

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-128.0016 872.9040

sample estimates:

mean in group boys mean in group girls

5907.098 5534.646

Based on the p-value, we cannot reject the null hypothesis that the true difference in means is equal to zero.

basicStats(abhutondot[-1])

boys girls

nobs 8.200000e+01 8.200000e+01

NAs 0.000000e+00 0.000000e+00

Minimum 2.890000e+03 2.722000e+03

Maximum 8.426000e+03 7.779000e+03

1. Quartile 4.759250e+03 4.457000e+03

3. Quartile 7.576500e+03 7.150250e+03

Mean 5.907098e+03 5.534646e+03

Median 6.073000e+03 5.718000e+03

Sum 4.843820e+05 4.538410e+05

SE Mean 1.825161e+02 1.758222e+02

LCL Mean 5.543948e+03 5.184815e+03

UCL Mean 6.270247e+03 5.884477e+03

Variance 2.731595e+06 2.534902e+06

Stdev 1.652754e+03 1.592137e+03

Skewness -2.139250e-01 -2.204720e-01

Kurtosis -1.221721e+00 -1.250893e+00

p1 <- ggplot(data = abhutondot_rs, aes(x = variable, y = value)) + geom_boxplot()

p2 <- ggplot(data = abhutondot, aes(boys)) + geom_density()

p3 <- ggplot(data = abhutondot, aes(girls)) + geom_density()

multiplot(p1, p2, p3, cols = 3)

Gives this plot.

Let us define the time series to be analysed with frequency = 1 as data is collected yearly, see ref. [5] for details.

excess_frac <- (abhutondot$boys - abhutondot$girls)/abhutondot$girls excess_ts <- ts(excess_frac, frequency = 1, start = abhutondot$year[1]) autoplot(excess_ts)

Gives this plot.

Basic statistics metrics are reported.

basicStats(excess_frac)

excess_frac

nobs 82.000000

NAs 0.000000

Minimum 0.010673

Maximum 0.156075

1. Quartile 0.048469

3. Quartile 0.087510

Mean 0.070748

Median 0.064704

Sum 5.801343

SE Mean 0.003451

LCL Mean 0.063881

UCL Mean 0.077615

Variance 0.000977

Stdev 0.031254

Skewness 0.680042

Kurtosis 0.073620

Boys births were at least 1% higher than girls ones, reaching a top percentage excess equal to 15%.

Further, unit roots tests (run by urdfTest() within fUnitRoots package) show that we cannot reject the null hypothesis of unit root presence. See their test statistics compared with critical values below (see ref. [2] for details about the urdfTest() report).

urdftest_lag = floor(12*(length(excess_ts)/100)^0.25)

urdfTest(excess_ts, type = "nc", lags = urdftest_lag, doplot = FALSE)

Title:

Augmented Dickey-Fuller Unit Root Test

Test Results:

Test regression none

Call:

lm(formula = z.diff ~ z.lag.1 - 1 + z.diff.lag)

Residuals:

Min 1Q Median 3Q Max

-0.052739 -0.018246 -0.002899 0.019396 0.069349

Coefficients:

Estimate Std. Error t value Pr(>|t|)

z.lag.1 -0.01465 0.05027 -0.291 0.771802

z.diff.lag1 -0.71838 0.13552 -5.301 1.87e-06 ***

z.diff.lag2 -0.66917 0.16431 -4.073 0.000143 ***

z.diff.lag3 -0.58640 0.18567 -3.158 0.002519 **

z.diff.lag4 -0.56529 0.19688 -2.871 0.005700 **

z.diff.lag5 -0.58489 0.20248 -2.889 0.005432 **

z.diff.lag6 -0.60278 0.20075 -3.003 0.003944 **

z.diff.lag7 -0.43509 0.20012 -2.174 0.033786 *

z.diff.lag8 -0.28608 0.19283 -1.484 0.143335

z.diff.lag9 -0.14212 0.18150 -0.783 0.436769

z.diff.lag10 0.13232 0.15903 0.832 0.408801

z.diff.lag11 -0.07234 0.12774 -0.566 0.573346

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.03026 on 58 degrees of freedom

Multiple R-squared: 0.4638, Adjusted R-squared: 0.3529

F-statistic: 4.181 on 12 and 58 DF, p-value: 0.0001034

Value of test-statistic is: -0.2914

Critical values for test statistics:

1pct 5pct 10pct

tau1 -2.6 -1.95 -1.61

urdfTest(excess_ts, type = "c", lags = urdftest_lag, doplot = FALSE)

Title:

Augmented Dickey-Fuller Unit Root Test

Test Results:

Test regression drift

Call:

lm(formula = z.diff ~ z.lag.1 + 1 + z.diff.lag)

Residuals:

Min 1Q Median 3Q Max

-0.051868 -0.018870 -0.005227 0.019503 0.067936

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.02239 0.01789 1.251 0.2159

z.lag.1 -0.31889 0.24824 -1.285 0.2041

z.diff.lag1 -0.44287 0.25820 -1.715 0.0917 .

z.diff.lag2 -0.40952 0.26418 -1.550 0.1266

z.diff.lag3 -0.34933 0.26464 -1.320 0.1921

z.diff.lag4 -0.35207 0.25966 -1.356 0.1805

z.diff.lag5 -0.39863 0.25053 -1.591 0.1171

z.diff.lag6 -0.44797 0.23498 -1.906 0.0616 .

z.diff.lag7 -0.31103 0.22246 -1.398 0.1675

z.diff.lag8 -0.19044 0.20656 -0.922 0.3604

z.diff.lag9 -0.07128 0.18928 -0.377 0.7079

z.diff.lag10 0.18023 0.16283 1.107 0.2730

z.diff.lag11 -0.04154 0.12948 -0.321 0.7495

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.03012 on 57 degrees of freedom

Multiple R-squared: 0.4781, Adjusted R-squared: 0.3683

F-statistic: 4.352 on 12 and 57 DF, p-value: 6.962e-05

Value of test-statistic is: -1.2846 0.8257

Critical values for test statistics:

1pct 5pct 10pct

tau2 -3.51 -2.89 -2.58

phi1 6.70 4.71 3.86

ACF and PACF plots are given.

par(mfrow=c(1,2)) acf(excess_ts) pacf(excess_ts)

Gives this plot:

We observe the auto-correlation spike at lag = 10 beyond confidence region. That suggests the presence of a seasonal component with period = 10. Structural changes are now investigated. First let us verify if regression against a constant is significative for our time series.

summary(lm(excess_ts ~ 1))

Call:

lm(formula = excess_ts ~ 1)

Residuals:

Min 1Q Median 3Q Max

-0.060075 -0.022279 -0.006044 0.016762 0.085327

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.070748 0.003451 20.5 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.03125 on 81 degrees of freedom

The intercept is reported as significative. Let us see if there are any structural breaks.

(break_point <- breakpoints(excess_ts ~ 1)) Optimal 2-segment partition: Call: breakpoints.formula(formula = excess_ts ~ 1) Breakpoints at observation number: 42 Corresponding to breakdates: 1670 plot(break_point)

Gives this plot.

summary(break_point) Optimal (m+1)-segment partition: Call: breakpoints.formula(formula = excess_ts ~ 1) Breakpoints at observation number: m = 1 42 m = 2 20 42 m = 3 20 35 48 m = 4 20 35 50 66 m = 5 17 30 42 56 69 Corresponding to breakdates: m = 1 1670 m = 2 1648 1670 m = 3 1648 1663 1676 m = 4 1648 1663 1678 1694 m = 5 1645 1658 1670 1684 1697 Fit: m 0 1 2 3 4 5 RSS 0.07912 0.06840 0.06210 0.06022 0.05826 0.05894 BIC -327.84807 -330.97945 -330.08081 -323.78985 -317.68933 -307.92410

The BIC minimum value is reached when m = 1, hence just one break point is determined corresponding to year 1670. Let us plot the original time series against its structural break and its confidence interval.

plot(excess_ts) lines(fitted(break_point, breaks = 1), col = 4) lines(confint(break_point, breaks = 1))

Gives this plot.

Boys vs girls sex ratio at birth changed from:

fitted(break_point)[1] 0.08190905

to:

fitted(breakpoint)[length(excess_ts)] 0.05902908

Running a t.test() to verify further the difference in mean is significative across the two time windows identified by the breakpoint date, year 1670.

break_date <- breakdates(break_point) win_1 <- window(excess_ts, end = break_date) win_2 <- window(excess_ts, start = break_date + 1) t.test(win_1, win_2) Welch Two Sample t-test data: win_1 and win_2 t = 3.5773, df = 70.961, p-value = 0.0006305 alternative hypothesis: true difference in means is not equal to 0 95 percent confidence interval: 0.01012671 0.03563322 sample estimates: mean of x mean of y 0.08190905 0.05902908

Based on reported p-value, we reject the null hypothesis that the true difference is equal to zero.

ARIMA Models

I am going to compare the following six ARIMA models (represented with the usual (p,d,q)(P,D,Q)[S] notation):

1. non seasonal (1,1,1), as determined by auto.arima() within forecast package 2. seasonal (1,0,0)(0,0,1)[10] 3. seasonal (1,0,0)(1,0,0)[10] 4. seasonal (0,0,0)(0,0,1)[10] with level shift regressor as intervention variable 5. seasonal (1,0,0)(0,0,1)[10] with level shift regressor as intervention variable 6. non seasonal (1,0,0) with level shift regressor as intervention variable

Here we go.

Model #1

The first model is determined by the auto.arima() function within the forecast package, using the options:

a. stepwise = FALSE, which allows for a more in-depth search of potential models

b. trace = TRUE, which allows to get a list of all the investigated models

Further, as default input to auto.arima() :

c. stationary = FALSE, so that models search is not restricted to stationary models

d. seasonal = TRUE, so that models search is not restricted to non seasonal models

(model_1 <- auto.arima(excess_ts, stepwise = FALSE, trace = TRUE))

ARIMA(0,1,0) : -301.4365

ARIMA(0,1,0) with drift : -299.3722

ARIMA(0,1,1) : -328.9381

ARIMA(0,1,1) with drift : -326.9276

ARIMA(0,1,2) : -329.4061

ARIMA(0,1,2) with drift : Inf

ARIMA(0,1,3) : -327.2841

ARIMA(0,1,3) with drift : Inf

ARIMA(0,1,4) : -325.7604

ARIMA(0,1,4) with drift : Inf

ARIMA(0,1,5) : -323.4805

ARIMA(0,1,5) with drift : Inf

ARIMA(1,1,0) : -312.8106

ARIMA(1,1,0) with drift : -310.7155

ARIMA(1,1,1) : -329.5727

ARIMA(1,1,1) with drift : Inf

ARIMA(1,1,2) : -327.3821

ARIMA(1,1,2) with drift : Inf

ARIMA(1,1,3) : -325.1085

ARIMA(1,1,3) with drift : Inf

ARIMA(1,1,4) : -323.446

ARIMA(1,1,4) with drift : Inf

ARIMA(2,1,0) : -317.1234

ARIMA(2,1,0) with drift : -314.9816

ARIMA(2,1,1) : -327.3795

ARIMA(2,1,1) with drift : Inf

ARIMA(2,1,2) : -325.0859

ARIMA(2,1,2) with drift : Inf

ARIMA(2,1,3) : -322.9714

ARIMA(2,1,3) with drift : Inf

ARIMA(3,1,0) : -315.9114

ARIMA(3,1,0) with drift : -313.7128

ARIMA(3,1,1) : -325.1497

ARIMA(3,1,1) with drift : Inf

ARIMA(3,1,2) : -323.1363

ARIMA(3,1,2) with drift : Inf

ARIMA(4,1,0) : -315.3018

ARIMA(4,1,0) with drift : -313.0426

ARIMA(4,1,1) : -324.2463

ARIMA(4,1,1) with drift : -322.0252

ARIMA(5,1,0) : -315.1075

ARIMA(5,1,0) with drift : -312.7776

Series: excess_ts

ARIMA(1,1,1)

Coefficients:

ar1 ma1

0.2224 -0.9258

s.e. 0.1318 0.0683

sigma^2 estimated as 0.0009316: log likelihood=167.94

AIC=-329.88 AICc=-329.57 BIC=-322.7

As we can see, all investigated models have d=1, which is congruent with the augmented Dickey-Fuller test results.

summary(model_1)

Series: excess_ts

ARIMA(1,1,1)

Coefficients:

ar1 ma1

0.2224 -0.9258

s.e. 0.1318 0.0683

sigma^2 estimated as 0.0009316: log likelihood=167.94

AIC=-329.88 AICc=-329.57 BIC=-322.7

Training set error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set -0.002931698 0.02995934 0.02405062 -27.05674 46.53832 0.8292635 -0.01005689

The significance of our (1,1,1) model coefficients is further investigated.

coeftest(model_1)

z test of coefficients:

Estimate Std. Error z value Pr(>|z|)

ar1 0.222363 0.131778 1.6874 0.09153 .

ma1 -0.925836 0.068276 -13.5603 < 2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Model #2

A spike at lag = 1 in the ACF plot suggests the presence of an auto-regressive component. Our second model candidate takes into account the seasonality observed at lag = 10. As a result, the candidate model (1,0,0)(0,0,1)[10] is investigated.

model_2 <- Arima(excess_ts, order = c(1,0,0),

seasonal = list(order = c(0,0,1), period = 10),

include.mean = TRUE)

summary(model_2)

Series: excess_ts

ARIMA(1,0,0)(0,0,1)[10] with non-zero mean

Coefficients:

ar1 sma1 mean

0.2373 0.3441 0.0708

s.e. 0.1104 0.1111 0.0053

sigma^2 estimated as 0.0008129: log likelihood=176.23

AIC=-344.46 AICc=-343.94 BIC=-334.83

Training set error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set -0.0002212383 0.02798445 0.02274858 -21.47547 42.96717 0.7843692 -0.004420048

coeftest(model_2)

z test of coefficients:

Estimate Std. Error z value Pr(>|z|)

ar1 0.2372975 0.1104323 2.1488 0.031650 *

sma1 0.3440811 0.1110791 3.0976 0.001951 **

intercept 0.0707836 0.0052663 13.4409 < 2.2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Model #3

In the third model, I introduce a seasonal auto-regressive component in place of the moving average one as present into model #2.

model_3 <- Arima(excess_ts, order = c(1,0,0),

seasonal = list(order = c(1,0,0), period = 10),

include.mean = TRUE)

summary(model_3)

Series: excess_ts

ARIMA(1,0,0)(1,0,0)[10] with non-zero mean

Coefficients:

ar1 sar1 mean

0.2637 0.3185 0.0705

s.e. 0.1069 0.1028 0.0058

sigma^2 estimated as 0.0008173: log likelihood=176.1

AIC=-344.19 AICc=-343.67 BIC=-334.56

Training set error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set -0.0002070952 0.02806013 0.02273145 -21.42509 42.85735 0.7837788 -0.005665764

coeftest(model_3)

z test of coefficients:

Estimate Std. Error z value Pr(>|z|)

ar1 0.2636602 0.1069472 2.4653 0.013689 *

sar1 0.3185397 0.1027903 3.0989 0.001942 **

intercept 0.0704636 0.0058313 12.0836 < 2.2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Model #4

This model takes into account the level shift highlighted by the structural change analysis and the seasonal component at lag = 10 observed in the ACF plot. To represent the structural change as level shift, a regressor variable named as level is defined as equal to zero for the timeline preceeding the breakpoint date and as equal to one afterwards such date. In other words, it is a step function which represents a permanent level shift. Such variable is input to the Arima() function as xreg argument. That is one of the most simple representation of an intervention variable, for a more complete overview see ref. [6].

level <- c(rep(0, break_point$breakpoints),

rep(1, length(excess_ts) - break_point$breakpoints))

model_4 <- Arima(excess_ts, order = c(0,0,0),

seasonal = list(order = c(0,0,1), period = 10),

xreg = level, include.mean = TRUE)

summary(model_4)

Series: excess_ts

Regression with ARIMA(0,0,0)(0,0,1)[10] errors

Coefficients:

sma1 intercept level

0.3437 0.0817 -0.0225

s.e. 0.1135 0.0053 0.0072

sigma^2 estimated as 0.0007706: log likelihood=178.45

AIC=-348.9 AICc=-348.38 BIC=-339.27

Training set error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set 0.0001703111 0.02724729 0.02184016 -19.82639 41.28977 0.7530469 0.1608774

coeftest(model_4)

z test of coefficients:

Estimate Std. Error z value Pr(>|z|)

sma1 0.3437109 0.1135387 3.0273 0.002468 **

intercept 0.0817445 0.0052825 15.4745 < 2.2e-16 ***

level -0.0225294 0.0072468 -3.1089 0.001878 **

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

The ‘level’ regressor coefficient indicates an average 2.2% decrease in the boys vs. girls excess birth ratio, afterwards year 1670.

Model #5

The present model adds to model #4 an auto-regressive component.

model_5 <- Arima(excess_ts, order = c(1,0,0),

seasonal = list(order = c(0,0,1), period=10),

xreg = level, include.mean = TRUE)

summary(model_5)

Series: excess_ts

Regression with ARIMA(1,0,0)(0,0,1)[10] errors

Coefficients:

ar1 sma1 intercept level

0.1649 0.3188 0.0820 -0.0230

s.e. 0.1099 0.1112 0.0061 0.0084

sigma^2 estimated as 0.0007612: log likelihood=179.56

AIC=-349.11 AICc=-348.32 BIC=-337.08

Training set error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set 8.225255e-05 0.02690781 0.02174375 -19.42485 40.90147 0.7497229 0.007234682

coeftest(model_5)

z test of coefficients:

Estimate Std. Error z value Pr(>|z|)

ar1 0.1648878 0.1099118 1.5002 0.133567

sma1 0.3187896 0.1112301 2.8660 0.004156 **

intercept 0.0819981 0.0061227 13.3926 < 2.2e-16 ***

level -0.0230176 0.0083874 -2.7443 0.006064 **

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

The auto-regressive coefficient ar1 is reported as not significative, hence this model is not taken into account further, even though it would provide a (very) slight improvement in the AIC metric.

Model #6

This model consideres the structural change as in model #4 without the seasonal component. That because I want to evaluate if any benefits comes from including a seasonal component.

model_6 <- Arima(excess_ts, order = c(1,0,0), xreg = level, include.mean = TRUE)

summary(model_6)

Series: excess_ts

Regression with ARIMA(1,0,0) errors

Coefficients:

ar1 intercept level

0.1820 0.0821 -0.0232

s.e. 0.1088 0.0053 0.0076

sigma^2 estimated as 0.0008369: log likelihood=175.68

AIC=-343.35 AICc=-342.83 BIC=-333.73

Training set error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set -7.777648e-05 0.02839508 0.02258574 -21.93086 43.2444 0.7787544 0.0003897161

coeftest(model_6)

z test of coefficients:

Estimate Std. Error z value Pr(>|z|)

ar1 0.1820054 0.1088357 1.6723 0.094466 .

intercept 0.0821470 0.0053294 15.4139 < 2.2e-16 ***

level -0.0232481 0.0076044 -3.0572 0.002234 **

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Models Residuals Analysis

It is relevant to verify if our models residuals are white noise or not. If not, the model under analysis has not captured all the structure of our original time series. For this purpose, I will take advantage of the checkresiduals() function within forecast package and the sarima() within the astsa package. What I like of the sarima() function is the residuals qqplot() with confidence region and the Ljung-Box plot to check significance of residuals correlations. If you like to further verify the Ljung-Box test results, I would suggest to take advantage of the LjungBoxTest() function within FitARMA package.

Notes:

1. Model #5 was taken out of the prosecution of the analysis, hence its residuals will not be checked.

2. checkresiduals() and sarima() gives textual outputs which are omitted as equivalent information is already included elsewhere. The checkresiduals() reports a short LjungBox test result. The sarima() function reports a textual model summary showing coefficients and metrics similar to already shown summaries.

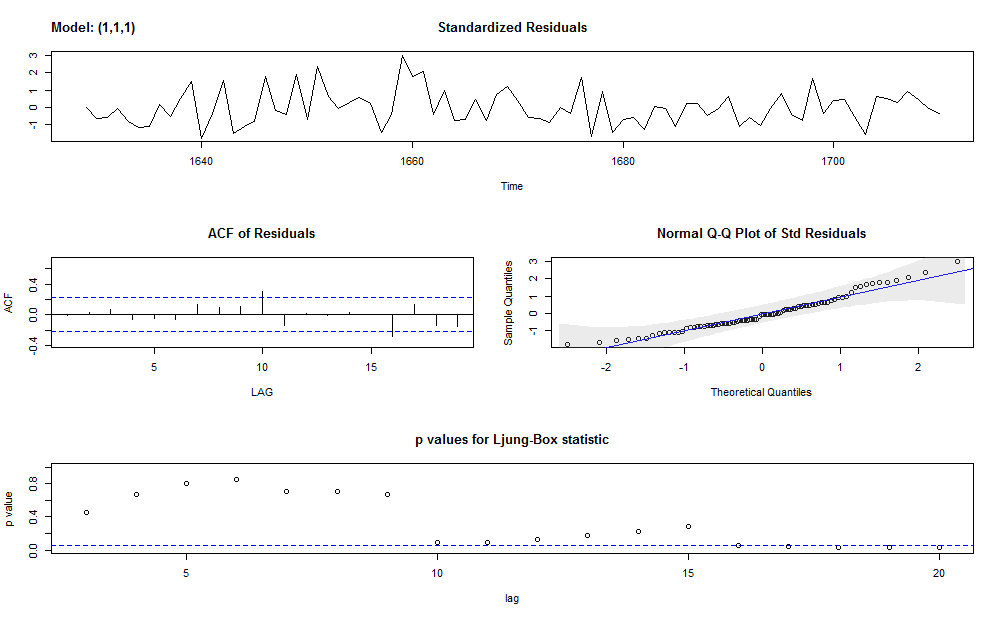

Model #1 Residuals Diagnostic

Checking ARIMA model (1,1,1) residuals.

checkresiduals(model_1)

Gives this plot.

It is important to verify the significance of residuals auto-correlation, in order to see if the spike at lag = 16 is as such. In fact, the purpose of running the LjungBox test is to verify if any auto-correlation beyond the confidence region (as seen in the ACF plot) is a true positive (p-value < 0.05) or is false positive (p-value >= 0.05).

LjungBoxTest(residuals(model_1), k = 2, lag.max = 20) m Qm pvalue 1 0.01 0.92611002 2 0.01 0.91139925 3 0.17 0.68276539 4 0.82 0.66216496 5 1.35 0.71745835 6 1.99 0.73828536 7 3.32 0.65017878 8 3.98 0.67886254 9 5.16 0.64076272 10 13.34 0.10075806 11 15.32 0.08260244 12 15.32 0.12066369 13 15.35 0.16692082 14 15.39 0.22084407 15 15.40 0.28310047 16 23.69 0.04989871 17 25.63 0.04204503 18 27.65 0.03480954 19 30.06 0.02590249 20 30.07 0.03680262

The p-value at lag = 16 is < 0.05 hence the auto-correlation spike at lag = 16 out of the confidence interval is significative. Our model #1 has not captured all the structure of the original time series. Also auto-correlations at lags = {17, 18, 19, 20} have p-value < 0.05, however they stand within the confidence inteval.

Now doing the same with sarima() function.

sarima(excess_ts, p = 1, d = 1, q = 1)

Gives this plot.

The sarima() output plot shows results congruent with previous comments.

Model #2 Residuals Diagnostic

Checking ARIMA (1,0,0)(0,0,1)[10] model residuals.

checkresiduals(model_2)

Gives this plot.

We observe how the model #2 does not show auto-correlation spikes above the confidence interval, and that is a confirmation of the presence of seasonality with period = 10.

LjungBoxTest(residuals(model_2), k = 2, lag.max = 20) m Qm pvalue 1 0.00 0.9674875 2 0.00 0.9545816 3 0.30 0.5815774 4 0.69 0.7096699 5 0.82 0.8442508 6 0.98 0.9121811 7 2.01 0.8481327 8 4.24 0.6442302 9 8.56 0.2861290 10 8.63 0.3742209 11 10.06 0.3459882 12 10.13 0.4290298 13 10.15 0.5172343 14 10.20 0.5985932 15 10.44 0.6577499 16 14.30 0.4275627 17 17.14 0.3104476 18 18.86 0.2759461 19 22.35 0.1715052 20 22.41 0.2142307

No p-value > 0.05 are shown by the LjungBox test report. Now showing sarima() plots.

sarima(excess_ts, p = 1, d = 0, q = 0, P = 0, D = 0, Q = 1, S = 10)

Gives this plot.

The sarima() output plot shows results congruent with previous comments. As a conclusion, model #2 has white noise residuals.

Model #3 Residuals Diagnostic

Checking ARIMA (1,0,0)(1,0,0)[10] model residuals.

checkresiduals(model_3)

Gives this plot.

LjungBoxTest(residuals(model_3), k = 2, lag.max = 20) m Qm pvalue 1 0.00 0.9583318 2 0.00 0.9553365 3 0.18 0.6719971 4 0.37 0.8313599 5 0.46 0.9285781 6 0.63 0.9600113 7 1.63 0.8975737 8 3.90 0.6901431 9 8.23 0.3126132 10 8.34 0.4005182 11 10.36 0.3222430 12 10.36 0.4091634 13 10.39 0.4960029 14 10.52 0.5708185 15 10.78 0.6290166 16 14.81 0.3914043 17 17.91 0.2675070 18 19.69 0.2343648 19 23.37 0.1374412 20 23.70 0.1651785 sarima(excess_ts, p = 1, d = 0, q = 0, P = 1, D = 0, Q = 0, S = 10)

Gives this plot.

Model#3 has white noise residuals.

Model #4 Residuals Diagnostic

Checking residuals of the ARIMA (0,0,0)(0,0,1)[10] model with level shift.

checkresiduals(model_4)

Gives this plot.

LjungBoxTest(residuals(model_4), k = 1, lag.max = 20) m Qm pvalue 1 2.20 0.1379312 2 2.23 0.1349922 3 2.24 0.3262675 4 3.68 0.2977682 5 4.99 0.2884494 6 5.23 0.3884858 7 5.52 0.4787801 8 7.45 0.3837810 9 10.78 0.2142605 10 10.79 0.2905934 11 12.61 0.2465522 12 12.61 0.3198632 13 12.61 0.3979718 14 12.63 0.4769589 15 12.65 0.5538915 16 16.37 0.3578806 17 16.77 0.4005631 18 19.73 0.2882971 19 25.25 0.1182396 20 25.31 0.1504763 sarima(excess_ts, p = 0, d = 0, q = 0, P = 0, D = 0, Q = 1, S = 10, xreg = level)

Gives this plot.

As a conclusion, model #4 has white noise residuals.

Model #6 Residuals Diagnostic

Checking residuals of the ARIMA (1,0,0) model with level shift.

checkresiduals(model_6)

Gives this plot

We can observe ACF spikes above the confidence region for lags = {10, 16}.

LjungBoxTest(residuals(model_6), k = 1, lag.max = 20) m Qm pvalue 1 0.00 0.99713258 2 0.00 0.96036600 3 0.07 0.96612792 4 1.51 0.67947886 5 2.70 0.60998895 6 4.47 0.48361437 7 5.20 0.51895133 8 5.49 0.59997164 9 6.51 0.58979614 10 14.72 0.09890580 11 17.09 0.07239050 12 17.21 0.10175761 13 17.21 0.14179063 14 17.24 0.18844158 15 17.34 0.23872998 16 25.31 0.04596230 17 27.53 0.03591335 18 29.50 0.03021450 19 31.47 0.02537517 20 31.71 0.03370585

The LjungBox test reports the residuals auto-correlation at lag = 10 as not signficative (p-value > 0.05). The lag = 16 residuals auto-correlation is significative (p-value < 0.05). Let us do same verifications with sarima().

sarima(excess_ts, p = 1, d = 0, q = 0, xreg = level)

Gives this plot.

The sarima() plots confirm the presence of significative auto-correlations in the residuals at lag = 16. As a conclusion, this model does not capture all the structure of our original time series.

As overall conclusion, only the seasonal models have white noise residuals.

Models Summary

Finally, it is time to gather the overall AIC, AICc and BIC metrics of our five candidate models (please remember that model #5 has been cut off from the prosecution of the analysis) and choose the final model.

df <- data.frame(col_1_res = c(model_1$aic, model_2$aic, model_3$aic, model_4$aic, model_6$aic),

col_2_res = c(model_1$aicc, model_2$aicc, model_3$aicc, model_4$aicc, model_6$aicc),

col_3_res = c(model_1$bic, model_2$bic, model_3$bic, model_4$bic, model_6$bic))

colnames(df) <- c("AIC", "AICc", "BIC")

rownames(df) <- c("ARIMA(1,1,1)",

"ARIMA(1,0,0)(0,0,1)[10]",

"ARIMA(1,0,0)(1,0,0)[10]",

"ARIMA(0,0,0)(0,0,1)[10] with level shift",

"ARIMA(1,0,0) with level shift")

df

AIC AICc BIC

ARIMA(1,1,1) -329.8844 -329.5727 -322.7010

ARIMA(1,0,0)(0,0,1)[10] -344.4575 -343.9380 -334.8306

ARIMA(1,0,0)(1,0,0)[10] -344.1906 -343.6711 -334.5637

ARIMA(0,0,0)(0,0,1)[10] with level shift -348.8963 -348.3768 -339.2694

ARIMA(1,0,0) with level shift -343.3529 -342.8334 -333.7260

The model which provides the best AIC, AICc and BIC metrics at the same time is model #4, ARIMA(0,0,0)(0,0,1)[10] with level shift.

Note: In case of structural changes, the (augmented) Dickey-Fuller test is biased toward the non rejection of the null, as ref. [2] explains. This may justify why the null hypothesis of unit root presence was not rejected by such test and model #1 performs worse than the other ones in terms of AIC metric. Further, you may verify that with d=1 in models from #2 up to #6, the AIC metric does not improve.

Forecast

I take advantage of the forecast() function provided within forecast package using model #4 as input. The xreg variable is determined as a constant level equal to one congruently with the structural analysis results.

h_fut <- 20 plot(forecast(model_4, h = h_fut, xreg = rep(1, h_fut)))

Gives this plot.

Historical Background

So we observed a level shift equal approximately to 2.25% in the boys vs girls births excess ratio occurring on year 1670. Two questions arises:

1. What could have influenced the sex-ratio at birth ?

2. What was happening in London during the 17-th century ?

There are studies showing results in support of the fact that sex-ratio at birth is influenced by war periods. Studies such as ref. [7], [8] and [9] suggest an increase of boys births during and/or after war time. General justification is for an adaptive response to external conditions and stresses. Differently, studies as ref. [10] state that there is no statistical evidence of war time influence on sex-ratio at births. Under normal circumstances, the boys vs girls sex ratio at birth is approximately 105:100 on average, (according to some sources), and generally between 102:100 and 108:100.

Our time series covers most of the following eras of the England history (ref. [11]):

* Early Stuart era: 1603-1660

* Later Stuart era 1660-1714

The English Civil War occured during the Early Stuart era and consisted of a series of armed conflicts and political machinations that took place between Parliamentarians (known as Roundheads) and Royalists (known as Cavaliers) between 1642 and 1651. The English conflict left some 34,000 Parliamentarians and 50,000 Royalists dead, while at least 100,000 men and women died from war-related diseases, bringing the total death toll caused by the three civil wars in England to almost 200,000 (see ref. [12]).

If we step back to view the first plot showing the abhutondot dataset, we can observe a sharp drop on births (both boys and girls) between 1642 and 1651, as testify a period of scarce resources and famine, and we can infer it was due to the civil war. Let us run a quick analysis on the total number of births.

abhutondot.ts <- ts(abhutondot$boys + abhutondot$girls, frequency = 1 ,

start = abhutondot$year[1])

autoplot(abhutondot.ts)

Gives this plot.

I then verify if any structural breaks are there with respect a constant level as regressor.

summary(lm(abhutondot.ts ~ 1))

Call:

lm(formula = abhutondot.ts ~ 1)

Residuals:

Min 1Q Median 3Q Max

-5829.7 -2243.0 371.3 3281.3 4703.3

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 11442 358 31.96 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 3242 on 81 degrees of freedom

The regression is reported as significative. Going on with the search for structural breaks, if any,

(break_point <- breakpoints(abhutondot.ts ~ 1)) Optimal 4-segment partition: Call: breakpoints.formula(formula = abhutondot.ts ~ 1) Breakpoints at observation number: 15 33 52 Corresponding to breakdates: 1643 1661 1680 plot(break_point)

Gives this plot.

summary(break_point)

Optimal (m+1)-segment partition:

Call:

breakpoints.formula(formula = abhutondot.ts ~ 1)

Breakpoints at observation number:

m = 1 39

m = 2 33 52

m = 3 15 33 52

m = 4 15 33 52 68

m = 5 15 32 44 56 68

Corresponding to breakdates:

m = 1 1667

m = 2 1661 1680

m = 3 1643 1661 1680

m = 4 1643 1661 1680 1696

m = 5 1643 1660 1672 1684 1696

Fit:

m 0 1 2 3 4 5

RSS 851165494 211346686 139782582 63564154 59593922 62188019

BIC 1566 1461 1436 1380 1383 1396

The BIC minimum value is reached with m = 3. Let us plot the original time series against its structural breaks and their confidence intervals.

plot(abhutondot.ts) fitted.ts <- fitted(break_point, breaks = 3) lines(fitted.ts, col = 4) lines(confint(break_point, breaks = 3))

Gives this plot.

The fitted levels and the breakpoints dates are as follows.

unique(as.integer(fitted.ts)) [1] 9843 6791 11645 14902 breakdates(break_point, breaks = 3) [1] 1648 1663 1676

So it is confirmed that the total number of births went through a sequence of level shift due to exogeneous shocks. The civil war is very likely determining the first break and its end the second one. It is remarkable the total births decrease from the 9843 level down to 6791 occurring around year 1648. As well remarkable, the level up shift happened on year 1663, afterwards the civil war end. The excess sex ratio structural break on year 1670 occurred at a time approximately in between total births second and third breaks.

The fitted multiple level shifts (as determined by the structural breaks analysis) can be used as intervention variable to fit an ARIMA model, as shown below.

fitted.ts <- fitted(break_point, breaks = 3) autoplot(fitted.ts)

Gives this plot.

abhutondot_xreg <- Arima(abhutondot.ts, order = c(0,1,1), xreg = fitted.ts, include.mean = TRUE)

summary(abhutondot_xreg)

Series: abhutondot.ts

Regression with ARIMA(0,1,1) errors

Coefficients:

ma1 fitted.ts

-0.5481 0.5580

s.e. 0.1507 0.1501

sigma^2 estimated as 743937: log likelihood=-661.65

AIC=1329.3 AICc=1329.61 BIC=1336.48

Training set error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set 71.60873 846.5933 622.1021 0.0132448 5.92764 1.002253 0.08043183

coeftest(abhutondot_xreg)

z test of coefficients:

Estimate Std. Error z value Pr(>|z|)

ma1 -0.54809 0.15071 -3.6368 0.0002761 ***

fitted.ts 0.55799 0.15011 3.7173 0.0002013 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

checkresiduals(abhutondot_xreg)

Gives this plot.

LjungBoxTest(residuals(abhutondot_xreg), k=1, lag.max=20) m Qm pvalue 1 1.39 0.2387836 2 2.26 0.1325458 3 2.31 0.3156867 4 2.69 0.4416912 5 2.93 0.5701546 6 3.32 0.6503402 7 4.14 0.6580172 8 4.53 0.7170882 9 4.54 0.8054321 10 7.86 0.5479118 11 8.51 0.5791178 12 8.54 0.6644773 13 8.69 0.7292904 14 9.31 0.7491884 15 11.16 0.6734453 16 11.50 0.7163115 17 12.58 0.7035068 18 12.60 0.7627357 19 13.01 0.7906889 20 14.83 0.7334703 sarima(abhutondot.ts, p=0, d=1, q=1, xreg = fitted.ts)

Gives this plot.

The residuals are white noise.

Conclusions

To have spot seasonality and level shifts were important aspects in our ARIMA models analysis. The seasonal component allowed to define models with white noise residuals. The structural breaks analysis allowed to define models with better AIC metric introducing as regressor the identified level shifts. We also had the chance to go through some historical remarks of the history of England and get to know about sex ratio at birth studies.

If you have any questions, please feel free to comment below.

References

- [1] Applied Econometrics with R, Achim Zeileis, Christian Kleiber – Springer Ed.

[2] Applied Econometrics Time Series, Walter Enders – Wiley Ed.

[3] Intervention Analysis – Penn State, Eberly College of Science – STAT510

[4] Forecast Package

[5] Seasonal Periods – Rob J. Hyndman

[6] Time Series Analysis With Applications in R – Jonathan D. Cryer, Kung.Sik Chan – Springer Ed.,

[7] Why are more boys born during war ? – Dirk Bethmann, Michael Kvasnicka

[8] Evolutionary ecology of human birth sex ratio – Samuli Helle, Samuli Helama, Kalle Lertola

[9] The Sex Ratio at Birth Following Periods of Conflict – Patrick Clarkin

[10] The ratio of male to female births as affected by wars – E. R. Shaw – American Statistical Association

[11] Early Modern Britain – Wikipedia

[12] English Civil Wars

Related Post

- A Gentle Introduction on Market Basket Analysis — Association Rules

- Building A Book Recommender System – The Basics, kNN and Matrix Factorization

- Explaining complex machine learning models with LIME

- Text Message Classification

- Analyzing Google Trends Data in R

R-bloggers.com offers daily e-mail updates about R news and tutorials about learning R and many other topics. Click here if you're looking to post or find an R/data-science job.

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.