Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.

Huge lines at gas stations have been seen around Turkey in recent days. Under the reason for this is the rise in the prices so often, in the last few months and the expectation to continue this. Of course, it is known that the rise in the exchange rate (US dollar to Turkish lira) has an important role in the hikes in gas prices. Considering the exchange currency crisis had been going on recently, it seems to be reasonable.

We will model the gas prices in terms of the exchange rate(xe), but this time, not only the current exchange rate but also, I want to add lagged values of xe to the model; Because the change of xe rates might not affect the prices immediately. Our model should be as below:

The dataset we are going to use is that from 2019 to the present, gas prices and xe rates. In the code block below, we build tsibble data frame object and separate it into the train and test set.

library(tidyverse)

library(tidymodels)

library(readxl)

library(tsibble)

library(fable)

library(feasts)

df <- read_excel("gasoline.xlsx")

#Building tsibble dataset

df_tsbl <- df %>%

mutate(date=as.Date(date)) %>%

as_tsibble() %>%

fill_gaps() %>% #makes regular time series by filling the time gaps

#fills in NAs with previous values

fill(xe,gasoline,.direction = "down")

#Separating into train and test set without random selection

#Takes first %75 for the training and the rest for the test set

df_split <- initial_time_split(df_tsbl, prop = 3/4)

df_train <- training(df_split)

df_test <- testing(df_split)

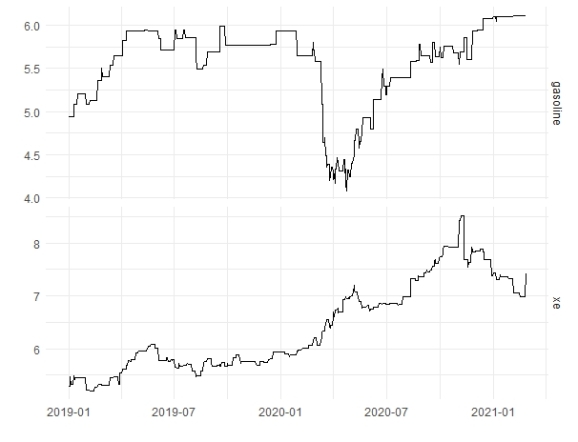

First of all, we will check the stationary of dependent and independent variables of the model as always.

#Checking the stationary

df_train %>%

pivot_longer(gasoline:xe) %>%

ggplot(aes(x=date,y=value))+

geom_line()+

facet_grid(vars(name),scales = "free_y")+

xlab("")+ylab("")+

theme_minimal()

It seems that it is better we make differencing the gas and xe variables.

#Comparing the probable lagged models

model_lags_diff <- df_train %>%

#Excludes the first three days so all versions are in the same time period

mutate(gasoline=c(NA,NA,NA,gasoline[4:788])) %>%

model(

lag0 = ARIMA(gasoline ~ pdq(d = 1) + xe),

lag1 = ARIMA(gasoline ~ pdq(d = 1) +

xe + lag(xe)),

lag2 = ARIMA(gasoline ~ pdq(d = 1) +

xe + lag(xe) +

lag(xe, 2)),

lag3 = ARIMA(gasoline ~ pdq(d = 1) +

xe + lag(xe) +

lag(xe, 2) + lag(xe, 3))

)

glance(model_lags_diff) %>%

arrange(AICc) %>%

select(.model:AICc)

# A tibble: 4 x 5

# .model sigma2 log_lik AIC AICc

# <chr> <dbl> <dbl> <dbl> <dbl>

#1 lag1 0.00310 1152. -2294. -2294.

#2 lag2 0.00311 1152. -2292. -2292.

#3 lag3 0.00311 1152. -2290. -2290.

#4 lag0 0.00313 1148. -2288. -2288.

By the AICc results, it is better to select the one-level lagged model.

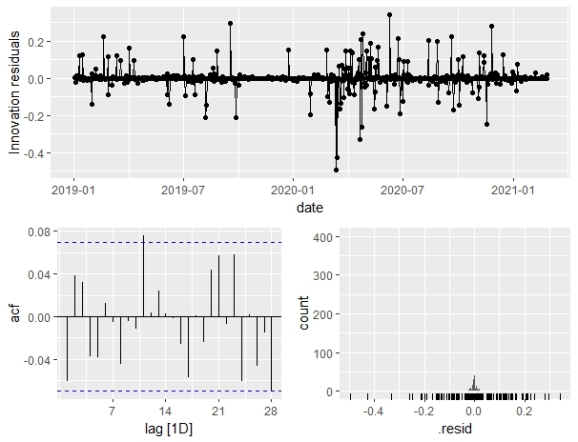

#Creates the model variable to the above results model_lag1 <- df_train %>% model(ARIMA(gasoline ~ pdq(d = 1) + xe + lag(xe))) #Checking the model residuals consistency with white noise model_lag1 %>% gg_tsresiduals()

All the spikes seem to be within the threshold line to the ACF plot, so the residuals can be considered white noise. So, we are comfortable with the model we chose.

report(model_lag1) #Series: gasoline #Model: LM w/ ARIMA(0,1,0)(2,0,0)[7] errors #Coefficients: # sar1 sar2 xe lag(xe) # 0.0920 0.1065 -0.0436 0.1060 #s.e. 0.0356 0.0359 0.0361 0.0368 #sigma^2 estimated as 0.003103: log likelihood=1155.84 #AIC=-2301.69 AICc=-2301.61 BIC=-2278.35

The above results indicate that the model has the weekly seasonal AR(1) and AR(2) components. Now, we will predict with the test set by using the above regression equations to assess the accuracy of our model.

#Lagged Forecasts model_pred <- forecast(model_lag1,df_test) #Accuracy of the lagged model cor(df_test$gasoline,model_pred$.mean) %>% round(2) #[1] 0.77

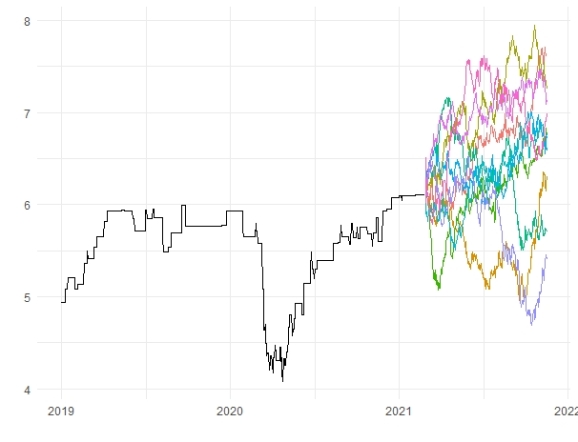

The result seems to be fine but we can try to improve it. In order to do that we will use bootstrapping and bagging methods.

set.seed(456)#getting the optimal and similar results for reproducibility

#Bootstrapped forecasts

sim_fc <- model_lag1 %>%

fabletools::generate(new_data=df_test,

times=10,

bootstrap_block_size=14) %>%

select(-.model)

#Drawing bootstrapped forecasts

sim_fc %>%

autoplot(.sim)+

autolayer(df_train,gasoline)+

guides(color="none")+

xlab("")+ylab("")+

theme_minimal()

#Bagged forecasts bagged_fc <- sim_fc %>% summarise(bagged_mean=mean(.sim)) #Accuracy of bagging model cor(df_test$gasoline,bagged_fc$bagged_mean) %>% round(2) #[1] 0.85

Quite a significant improvement for the accuracy of our model; it seems the bootstrapping simulation works in this process.

R-bloggers.com offers daily e-mail updates about R news and tutorials about learning R and many other topics. Click here if you're looking to post or find an R/data-science job.

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.