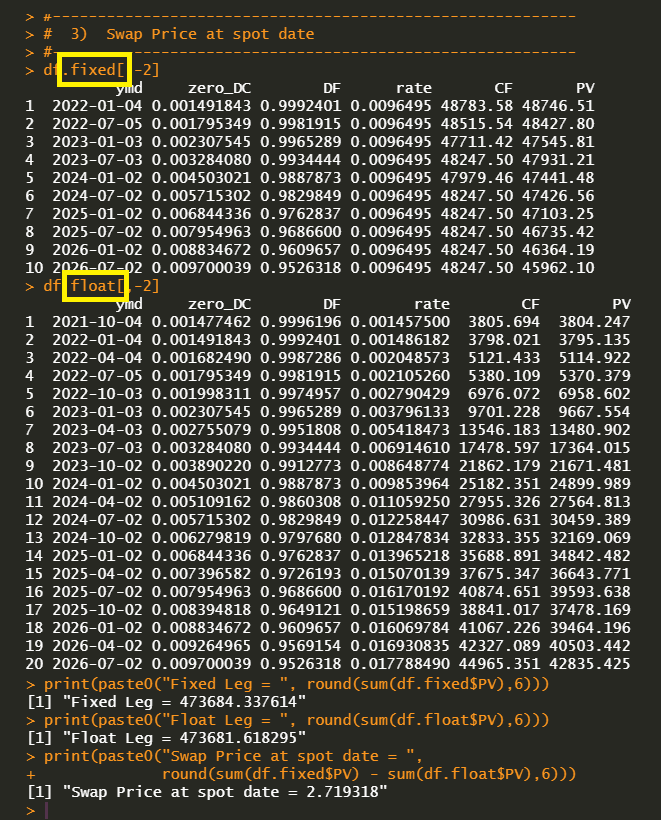

This post explains how to price an interest rate swap (IRS) using R code and Excel’s illustrations. We use swap rates, zero curve data from Bloomberg. We consider 5-Year Libor 3M IRS without OIS discounting as an pre-crisis IRS example. Libor …