Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.

Here are the slides of the talk that I gave yesterday with Prof. Frédéric Planchet at the 8th Rmetrics workshop in Insurance and Finance :

The R codes can found here :

- For ESG

- For ESGtoolkit

I also submitted (a bit late, maybe) a Shiny app for the Shiny App contest (which is the example @ page 55 of the slides).

https://contest.shinyapps.io/ShinyALMapp/

The username is : contest.

The password : rmetrics.

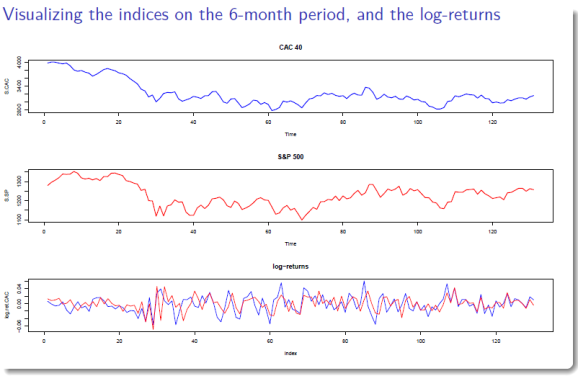

However, in my opinion, my app is veerry slow. This is due to the way that I dealt with global/local variables. In the first section, ‘Simulation’, I make projections of the portfolio assets, let’s call the associated R variables : S.CAC and S.SP. In server.R, the plot is obtained with output$plotSimulation. In the second section, ‘Portfolio’, I had to duplicate the code for the simulation (veerry annoying… here’s the bottleneck), because S.CAC and S.SP could’nt be seen in the scope of output$plotPortfolio defined in server.R.

I didn’t have the time to investigate more by now. But If somebody knows how to deal with this in Shiny, I’ll be happy to hear !

R-bloggers.com offers daily e-mail updates about R news and tutorials about learning R and many other topics. Click here if you're looking to post or find an R/data-science job.

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.