Down and Dirty Forecasting: Part 2

[This article was first published on OutLie..R, and kindly contributed to R-bloggers]. (You can report issue about the content on this page here)

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.

This is the second part of the forecasting exercise, where I am looking at a multiple regression. To keep it simple I chose the states that boarder WI and the US unemployment information for the regression. Again this is a down and dirty analysis, I would not call this complete in any sense.Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.

#getting the data for WI, US, IL, MI, MN, IO

#Using Quandl data, great little site

wi<-read.csv('http://www.quandl.com/api/v1/datasets/FRED/WIUR.csv?&auth_token=gigXwpxd6Ex91cjgz1B7&trim_start=1976-01-01&trim_end=2013-04-01&sort_order=desc', colClasses=c('Date'='Date'))

us<-read.csv('http://www.quandl.com/api/v1/datasets/FRED/UNRATE.csv?&auth_token=gigXwpxd6Ex91cjgz1B7&trim_start=1976-01-01&trim_end=2013-04-01&sort_order=desc', colClasses=c('Date'='Date'))

il<-read.csv('http://www.quandl.com/api/v1/datasets/FRED/ILUR.csv?&auth_token=gigXwpxd6Ex91cjgz1B7&trim_start=1976-01-01&trim_end=2013-04-01&sort_order=desc', colClasses=c('Date'='Date'))

mi<-read.csv('http://www.quandl.com/api/v1/datasets/FRED/MIUR.csv?&auth_token=gigXwpxd6Ex91cjgz1B7&trim_start=1976-01-01&trim_end=2013-04-01&sort_order=desc', colClasses=c('Date'='Date'))

mn<-read.csv('http://www.quandl.com/api/v1/datasets/FRED/MNUR.csv?&auth_token=gigXwpxd6Ex91cjgz1B7&trim_start=1976-01-01&trim_end=2013-04-01&sort_order=desc', colClasses=c('Date'='Date'))

io<-read.csv('http://www.quandl.com/api/v1/datasets/FRED/IAUR.csv?&auth_token=gigXwpxd6Ex91cjgz1B7&trim_start=1976-01-01&trim_end=2013-04-01&sort_order=desc', colClasses=c('Date'='Date'))

#merging the data into one dataframe

#I started with WI so that I could isolate the rest of the variables better

unemp<-merge(wi, io, by='Date'); colnames(unemp)<-c('Date', 'wi', 'io')

unemp<-merge(unemp, mi, by='Date'); colnames(unemp)<-c('Date', 'wi', 'io', 'mi')

unemp<-merge(unemp, mn, by='Date'); colnames(unemp)<-c('Date', 'wi', 'io', 'mi', 'mn')

unemp<-merge(unemp, us, by='Date'); colnames(unemp)<-c('Date', 'wi', 'io', 'mi', 'mn', 'us')

unemp<-merge(unemp, il, by='Date'); colnames(unemp)<-c('Date', 'wi', 'io', 'mi', 'mn', 'us', 'il')

save(unemp, file='Unemployment WI.RData')

library(car)

library(lmtest)

library(forecast)

load('Unemployment WI.RData')

unemp.b<-unemp[1:436,]

unemp.p<-unemp[437:448,]

plot(unemp$Date, unemp$us, col='black',

main='Unemployment WI Region', type='l', xlab='Date',

ylab='Unemp. Rate', ylim=c(2, 17))

lines(unemp$Date, unemp$il, col='blue')

lines(unemp$Date, unemp$io, col='dark green')

lines(unemp$Date, unemp$mi, col='purple')

lines(unemp$Date, unemp$mn, col='gray')

lines(unemp$Date, unemp$wi, col='red')

leg.txt<-c('US', 'IL', 'IO', 'MI', 'MN', "WI")

leg.col<-c('black','blue', 'dark green', 'purple', 'gray', 'red')

legend('topleft', leg.txt, col=leg.col, pch=15)

summary(unemp)

#correlation matrix

cm<-cor(unemp[,-1])

cm

#From the graph and correlation matrix, everything

#is highly correlated, the lowest r value is 0.7879

#between Iowa and US.

#plots of each of the data, then each individual,

#everything looks really good, nice linear trends,

#although Michigan has quite bit of volatility

#compared to the other variables.

plot(unemp.b, pch='.')

model<-lm(wi~., data=unemp.b[,-1])

step.m<-step(model, direction='backward')

summary(step.m)

#testing for outliers

outlierTest(step.m)

# After conducting the outlier test, looks like it is michigan

#Sept 1980 where unemployment was 13.2 percent, point 57 is

#close at 12.9 those are the two biggest, but the outlierTest

#isolated row 56

dwtest(step.m)

dwtest(step.m, alternative='two.sided')

#yep lots of autocorrelation, so a multiple ARAIMA might be in order

pred<-unemp.p[3:7]

mult.f<-predict(step.m, newdata=pred, interval='prediction')

a1<-accuracy(mult.f, unemp.p$wi)

#because the MASE is missing I needed to add the following to compare later

a1<-c(a1,'0')

names(a1)<-c("ME", "RMSE", "MAE", "MPE", "MAPE", "MASE")

# ARIMA

auto.r<-auto.arima(unemp.b$wi, xreg=unemp.b[,3:7])

auto.r

auto.f<-forecast(auto.r, xreg=unemp.p[,3:7], h=12)

a2<-accuracy(auto.f, unemp.p$wi)

a2

#Just remember that the 0 is just a place holder

r.table<-rbind(a1, a2)

row.names(r.table)<-c('Multiple Regression', 'Reg. with ARIMA Errors')

r.table

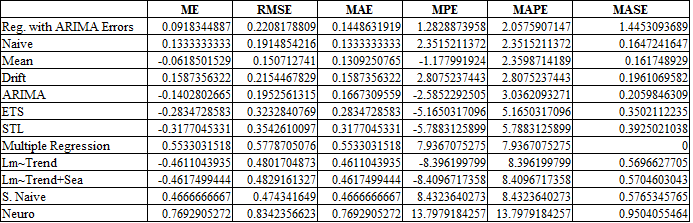

At this point I combined the two accuracy tables to see which one was the best.

b.table<-rbind(a.table[,1:6], r.table)

b.table<-b.table[order(b.table$MAPE),]

b.tableThe winner is: Regression with ARIMA Errors, for most of the analysis the simple mean like predictions dominated, even the multiple regression is considerably low on the list.

To leave a comment for the author, please follow the link and comment on their blog: OutLie..R.

R-bloggers.com offers daily e-mail updates about R news and tutorials about learning R and many other topics. Click here if you're looking to post or find an R/data-science job.

Want to share your content on R-bloggers? click here if you have a blog, or here if you don't.